Rocket Lab: Where I Was Wrong

Revisiting the vertical monopoly thesis at $72 billion

Like seemingly everybody in 2020, I started a YouTube channel. On that channel, I posted videos breaking down different kinds of companies, talking about investing, and occasionally teaching you how to build financial models. Some of those videos were on a company called Rocket Lab.

I have always been a fan of space, and I have always been a fan of investing. Rocket Lab caught my fancy. I pondered what could happen to this SPAC that had recently gone public and was being beat down along with every single other SPAC at the time. I saw a great future ahead for the company.

My problem was, especially if you look at some of the comments on the original video, I was far too conservative. I even had to defend a couple of my positions on Reddit, saying, “Hey, if I am too conservative, predicting here a more than 100% return in stock, then that is incredible.”

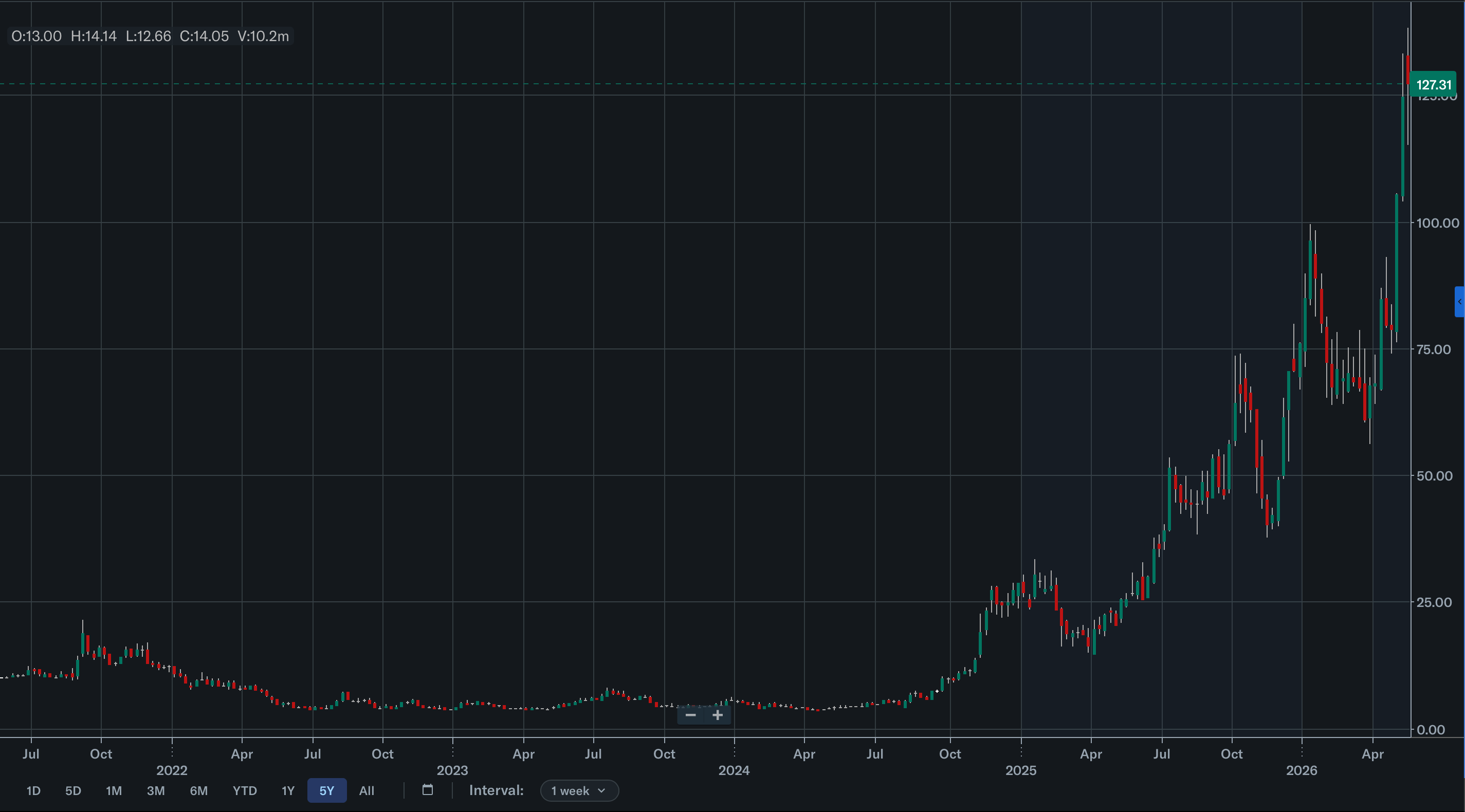

Rocket Lab has returned more than 3,000% since I made those videos saying that I was buying. My only problem right now is I wish I had bought more.

Here we are. I am writing this in May 2026. We are going to start out, right here on SpaceBreakdowns, with a deep dive into Rocket Lab. What has changed about Rocket Lab over the past few years, what the future looks like, and whether at $120 plus per share there is still room to run in this name, or whether it is finally time to sell.

Where Past Analysis Was Incorrect

In April 2024, I told you that excellent execution would yield a $20 stock. I was wrong. I modeled a traditional industrial business, but Peter Beck built an unassailable vertical monopoly. My models caught the trend, but missed the scale of institutional premium that we see today.

The Multiples Trap

In the April 2024 video linked here, I arrived at a long-term target price of $20 per share, assuming Rocket Lab had excellent execution. If Rocket Lab ended up at $20 a share now, I would be mind blown and extremely disappointed.

My thinking back then was that Rocket Lab should be modeled like a traditional high-growth industrial hardware company that would face multiple compression as its capital expenditure scaled. Instead, the market gave Rocket Lab a software-style scarcity premium, which is completely fair.

It is fair because Rocket Lab emerged as the only functional Western alternative to SpaceX. Wall Street threw standard EBITDA multiples out the window and re-rated them as a tier 1 national security asset. At $120 plus per share, I was wrong because I assumed the market would remain rational about valuation multiples for a hardware monopoly.

The Neutron Pricing Floor

In the first video I made about Rocket Lab in January 2024, I caught a lot of flak in the comments for modeling Neutron at a hyper-conservative $30 million per launch. The same feedback was on Reddit posts, and I made a second video that reran the numbers at the full $50 million retail price just to see the upside.

This was wrong, because even at $50 million, the model is treating launch as a static, commoditized line item. What actually happened by 2026 is that Rocket Lab began commanding premium block deals and National Security Space Launch phase 3 task orders. These defense missions do not just pay for the freight, they pay massive high margin premiums for custom orbit insertion, mission integration, and secure payload handling.

Rocket Lab being able to integrate all these parts was called out in those previous videos, but I never did acknowledge the value that would have on the pricing of Neutron.

Velocity and Margins of Space Systems

I correctly identified that Space Systems was the secret weapon, but I underestimated the sheer velocity of Rocket Lab’s vertical integration strategy.

By aggressively swallowing up the supply chain, capping it off with major moves like the Motiv and Mynaric integrations, Rocket Lab has turned space systems into an end-to-end captive powerhouse.

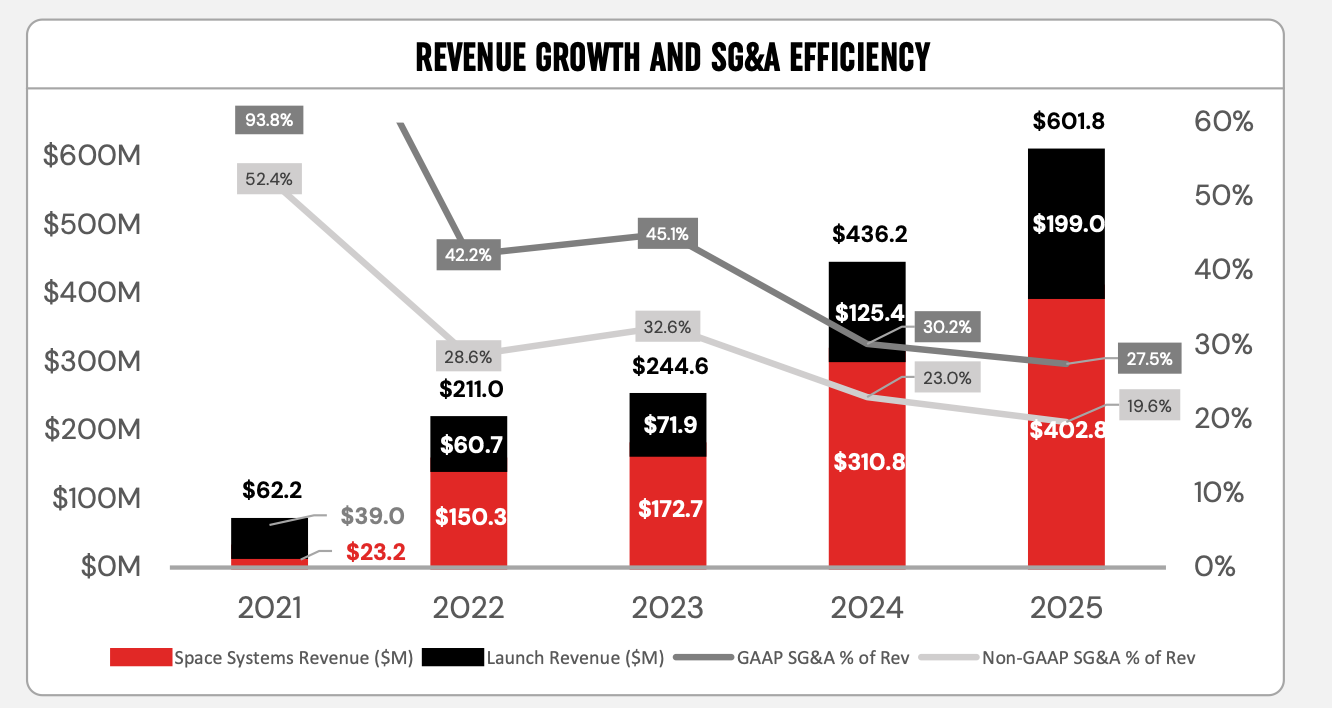

To be fair to my own modeling, I don’t believe anybody in early 2024 was modeling a 200 million dollar single quarter revenue run rate with 38.2% GAAP gross margins this early in the cycle.

Rocket Lab has very quickly ceased just being a component vendor and has become a prime contractor much sooner than expected.

The Q1 2026 Setup

I do not think there is any dispute that Rocket Lab had a fantastic Q1. The company had record revenue of $200.3 million. They now have a record backlog of $2.2 billion. They were able to sign 5 Neutron launches, and that manifest is now filling up through the end of the decade.

In addition, there were 31 Electron and HASTE missions booked, which is the highest booking Rocket Lab has ever had in a single quarter.

So far in 2026, there have been 8 launches year to date, and there are 70 more in the backlog. The 100th Electron launch for Rocket Lab should occur this year. There have been big partnerships with the likes of the Department of War, which signed a new launch contract for HASTE, and partnerships with Anduril to deliver new hypersonic capabilities for their national security program.

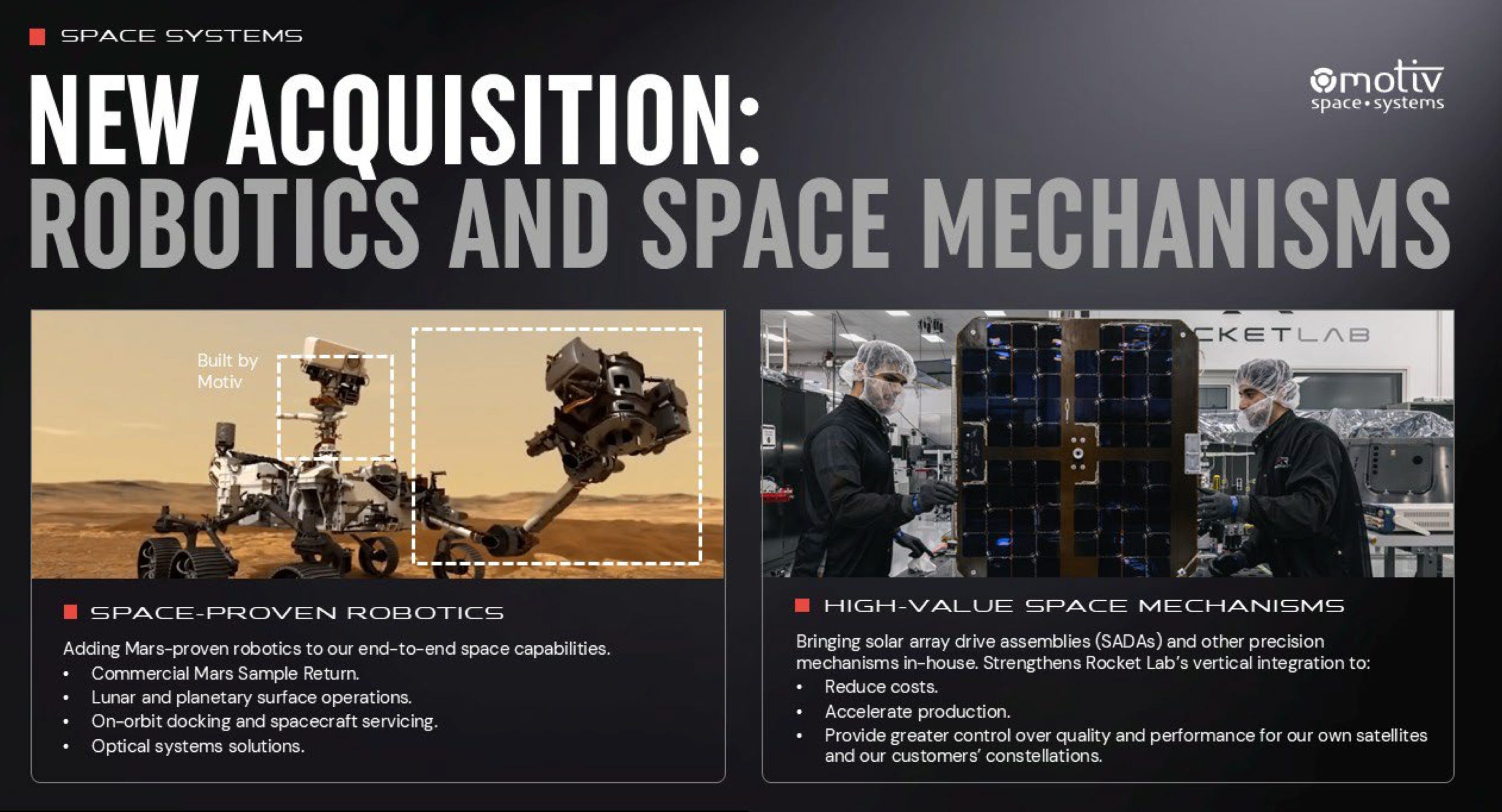

The key thing to pull out is the acquisition of the company Motiv and the completion of the Mynaric acquisition. Both of these acquisitions help expand how far Rocket Lab’s vertical integration can go.

Motiv brings space-proven robotics to the company’s offerings. As the company behind the Mars Perseverance Rover’s robotic arm and CADRE lunar rovers, they have put robotics systems on other planets that have been usable. This capability will now be available to Rocket Lab customers.

Along with robotics, Rocket Lab also added 7 new high-value products to its space systems lineup:

Electric propulsion, known as Gauss, which is a new in-house developed system for high-volume production

Optical payloads

Laser comms

Silicon solar

Star trackers

Robotics

Precision mechanisms

A popular line from Peter Beck is, “He who owns the payload owns the mission.” We can see from the steps Rocket Lab is taking that this is becoming more true over time. It is not new that Rocket Lab is trying to become the vertical integration play of space, but it is expanding how large that vertical offering actually is.

Over the years since I started covering Rocket Lab, it has gone from something that could put a satellite into space to a company where you can go and say, Hey, I want to build a robot that will go digging on Mars. Can you help me with that? And the answer is yes, 100%.

Rocket Lab can now design that robot, launch that robot, deploy that robot, and monitor and maintain that robot. All you need is the idea and the money to make it happen, and Rocket Lab will do that for you.

Overall, it was a fantastic quarter for Rocket Lab. They are the dominant Western alternative to SpaceX. SpaceX is the 1,000-pound gorilla in the room, but Rocket Lab is showing that they have the ability to be a major space company right alongside SpaceX. They may not dominate launch like SpaceX, but they are tackling a piece of the puzzle that nobody else is. That in itself is valuable.

The Bull Case

At the time of writing, Rocket Lab is a $72B company. You do not have to look back that far in the past to a time when it was a $10B company. To have gone from those levels up to $70B in such a short time is incredible.

At those levels, Rocket Lab is trading at approximately 25x forward 2027 revenue. The question is not whether that is expensive in absolute terms, as it obviously is. The question is whether Rocket Lab can continue to grow from these levels and prove that it is a company that is worth that much.

While we are not making buy or sell recommendations as part of this publication, it is worth talking about the price of Rocket Lab for just a minute. There are, I believe, 3 pillars that justify the valuation Rocket Lab is trading at today.

Pillar 1: Neutron

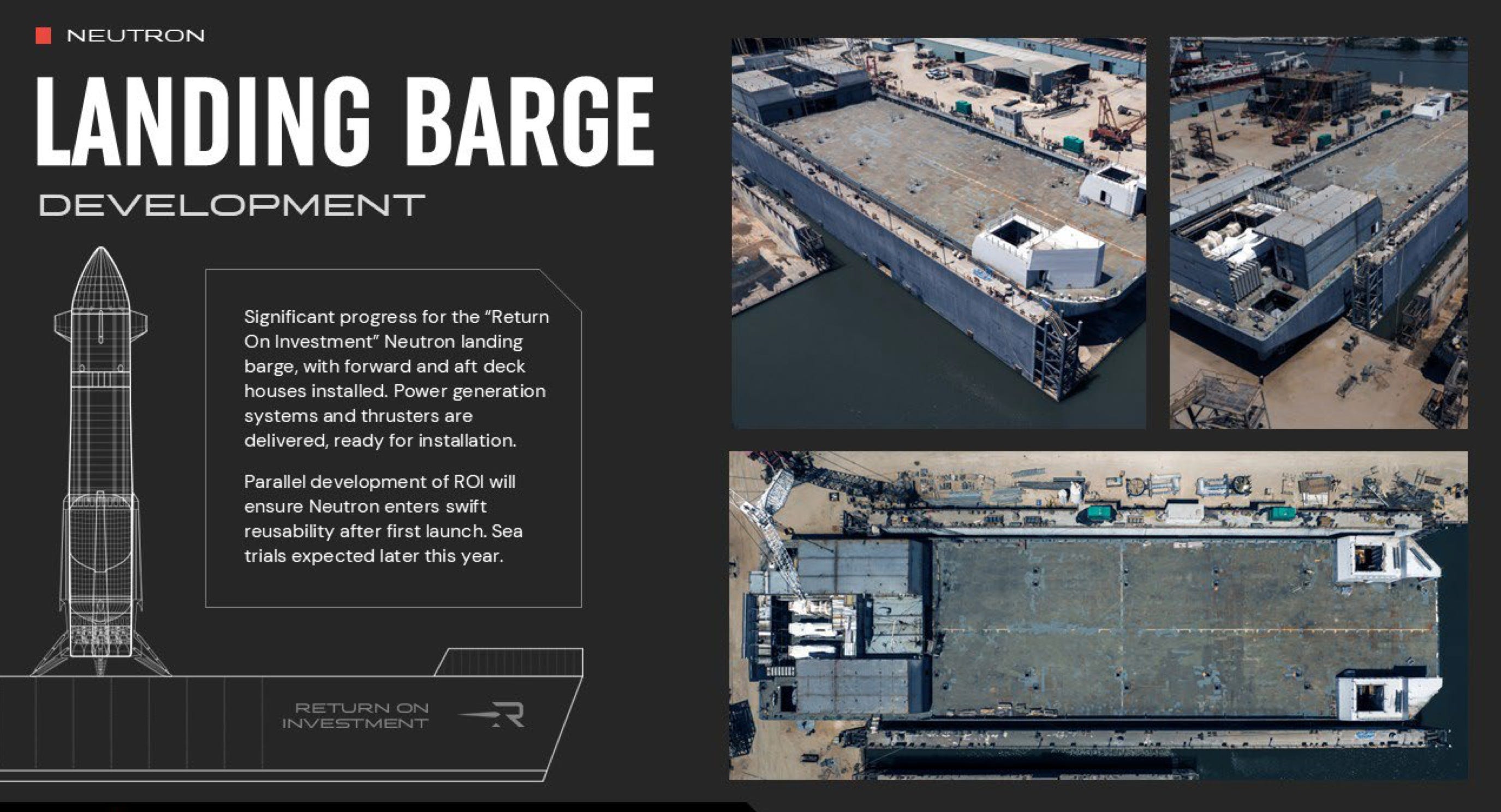

The first pillar is, of course, Neutron. Neutron is the shiny new thing and rightfully so. It is Rocket Lab’s medium-lift, partially reusable rocket that’s designed to put 13,000 kg into low Earth orbit. Makes it a direct competitor to SpaceX’s Falcon 9. A first launch is currently expected no earlier than the last quarter of 2026. The first stage is designed to be recovered on an ocean barge that they’re calling Return On Investment, for reuse.

Now Neutron matters but it’s not just for the launch revenue. The biggest story around Neutron for me is the flywheel. If you are a customer coming to Rocket Lab for a medium-lift launch, you are already more likely to use their components on your satellite. You’re more likely to use their software and you’re more likely to integrate with their broader space systems offering.

The inverse of that is also true. If you are already a Rocket Lab Space Systems customer, the launch decision becomes a natural fit. Neutron is not just a rocket; it is the gateway product that pulls everything else through.

This is a meaningful difference between Rocket Lab and a traditional launch provider. Rocket Lab is not selling Neutron the way ULA sells Vulcan or Arianespace sells the Ariane 6. They are selling Neutron as part of a bundle that competes on integration rather than just pure price per kilogram.

Pillar 2: Space Systems, The Prime

The second pillar is the one I underestimated the most in my early modeling. Rocket Lab is fast becoming the prime contractor for getting to space. If you have an idea for a mission, you go to Rocket Lab. It will design the satellite, build the components, integrate the payload, launch the rocket, and operate the spacecraft in orbit.

The Motiv acquisition is the move that crystallizes this thesis. Motiv built the robotic arm on NASA’s Perseverance rover and is delivering hardware for the CADRE lunar rovers. Rebranded as Rocket Lab Robotics, this isn’t just a component-supplier acquisition; it’s a full-on credentials acquisition. Rocket Lab can now credibly bid as a prime on planetary missions that previously belonged to JPL contractors and legacy primes. You combine that with the Mynaric acquisition for laser communications and the introduction of seven new high-value products in their space systems line up in Q1. Rocket Lab has closed most of the remaining gaps in their vertical integration play.

Peter Beck has always been explicit about the playbook: “Our acquisition strategy is simple but proven and effective. We identify the best space technologies that have struggled to scale and we bring them into the Rocket Lab ecosystem. By applying our resources, expertise, and manufacturing scale, we make these technologies more accessible and affordable for the global space industry.”

The Motiv deal is Rocket Lab’s seventh acquisition since 2020. Seven acquisitions in five years is not a side project. It’s a deliberate roll-up strategy that is aimed at making Rocket Lab the only place you need to go if you want to get to space.

If Rocket Lab succeeds in becoming the default prime for space access (in the same way that Heico became the default prime for aerospace replacement parts), the addressable market is substantially larger than launch alone. Space Systems revenue is growing faster than launch revenue. It carries a higher margin and benefits from the kind of switching costs that pure launch businesses alone do not have.

Pillar 3: Flatellite and the Constellation Play

The pillar 3 is the fun one and it’s the one that most people do not seem to be pricing in or talking about with Rocket Lab. In 2025, Rocket Lab announced Flatellite. It’s a flat stackable mass-producible satellite that is designed for large constellations. Beck himself described it as “a bold strategic move toward Rocket Lab operating its own constellation and delivering services from space.”

And Rocket Lab has rarely been shy about indicating that they will build their own constellation one day. Reporting from SatNews suggests that Flatellite is being aimed at 5G non-terrestrial networks, with industry chatter putting the minimum viable constellation in the 150 to 200 satellite range rather than the thousands required for Starlink-class build out. Beck’s own framing is: “By having our own rides to space with Neutron and Electron and being able to build our own spacecraft in high volumes, we have a distinct advantage when it comes to deploying constellations with speed and cost efficiency.”

To return to a quote we have earlier in the article, “He who owns the payload owns the mission.” The natural endpoint then of Rocket Lab’s vertical integration strategy is not just providing the rocket, the components, the spacecraft, and the operations to other people. It is operating its own services from space and capturing the revenue that flows to constellation operators rather than to their suppliers.

And this is obviously the part of the story that is hardest to value because it is the furthest from today’s revenue but it’s also the part that justifies multiples that look insane today. Starlink is on track to do somewhere in the neighborhood of $12 billion in revenue this year. If Rocket Lab can build even a meaningful niche position in 5G non-terrestrial networks over the next decade, that is not a $70 billion company. It is something much larger.

Of course the competition is real. Starlink dominates, Kuiper is coming, AST Space Mobile is in the market but this planet is large. The demand for connectivity is growing and the regulatory and capital barriers favor companies that already have the launch and manufacturing infrastructure in place. Rocket Lab is one of perhaps four companies in the world that can credibly stand up a constellation from scratch.

The Bear Case

There is a lot of expectation riding on Rocket Lab at these levels. At roughly 25x forward 2027 revenue, the market is pricing in flawless execution on three separate fronts that all still carry meaningful risk. Anyone that is buying or holding Rocket Lab at $120 plus per share owes themselves an honest accounting of what could go wrong.

Neutron Slippage

The most obvious risk is that Neutron slips again. The rocket was originally targeted for a 2024 launch that moved to 2025. It then moved to Q1 2026 after a stage one propellant tank ruptured during the hydrostatic test in January 2026. The first launch is now expected no earlier than the last quarter of 2026, with some analysts arguing that even that timeline looks optimistic.

Neutron development is not cheap. Spice, the Rocket Lab CFO, disclosed on the Q3 2025 earnings call that the company will have spent approximately $360 million on Neutron development through the end of 2025, with workforce costs running about $15 million per quarter. The original development estimate was $250 million to $300 million. That overrun is meaningful for a company that is not yet profitable.

Every quarter that Neutron slips is a quarter where Rocket Lab burns development cash without booking the launch revenue that justifies the investment. It is also a quarter where the NSSL lane 1 onramp gets pushed, where commercial Neutron manifests back up, and where the multiple compression risk increases. If Neutron does not fly until 2027, the bull case has to absorb a year of additional cash burn against a flat revenue ramp on the launch side.

Reusability is hard

SpaceX makes it look easy but the reality is that reusability is hard. Only two companies have ever landed and re-flown an orbital-class booster: SpaceX and Blue Origin. As SpaceX took years and many failures to make Falcon 9 reuse reliable, Blue Origin’s New Glenn has flown but is still early in its reuse program. Reusability is not a checkbox. It’s an engineering capability that takes dozens of flights to mature and it is part of the unit economics that justify Neutron’s $50 million price point.

If Neutron’s first stage proves harder to recover and refurbish than expected, if methalox cleanliness advantage is smaller than expected, if the canard and landing leg system has stability issues, if turnaround times stretch to months rather than weeks, then the economics of Neutron quickly deteriorate. A Neutron business case is heavily leveraged to reuse. Expendable Neutron is a much harder sell against the mature and reusable Falcon 9.

Scarcity Premium Can Evaporate

A lot of what is driving Rocket Lab’s premium valuation and SpaceX is scarcity. Rocket Lab is considered the only functional Western alternative to SpaceX and that scarcity justifies multiples that would not apply to a normal industrial hardware business.

And scarcity premiums are real but they are also very fragile. They depend on a competitive landscape being static and space is not static.

There’s Blue Origin’s New Glenn that flew successfully in 2025. It is ramping production. There’s Stoke’s Nova vehicle, targeting full reusability, with an architecture that, if it works, has better unit economics than Neutron. Relativity’s Terran R is in development. Firefly has an MLV in development with Northrop Grumman. ULA has the Vulcan, which is now operational. None of these are guaranteed to succeed but the field of medium-lift competitors is meaningfully larger today than it was when the market re-rated Rocket Lab.

If even two of these programs reach operational cadence over the next three years, Rocket Lab is no longer the only functional Western alternative to SpaceX. It ends up being one of several. At that point the scarcity premium would compress and Rocket Lab gets valued like a normal aerospace hardware business with a strong space systems franchise, which is real and a good business. It likely does not stay valued at 25x forward revenue.

The Verdict

Rocket Lab today is a different company than it was when I first covered it in 2024. A 3,000% return for investors reflects real operational achievement, record revenue, record backlog, the only functional Western alternative to SpaceX in development on Neutron, and a vertical integration strategy that has executed on seven acquisitions in five years and is now closing the final gaps in the stack.

At the same time, the valuation has run ahead of fundamentals in ways that require flawless execution to justify:

Neutron has to fly

re-use has to work

scarcity premium has to hold against a growing field of competitors

and the SpaceX IPO has to land well for the sector

Any one of those breaking lowers the multiple. Two of them breaking would compress it significantly.

The honest framing is that Rocket Lab today is no longer the asymmetric setup it was at $4, $10, or even $30 a share. The risk/reward has changed. The bull case is intact and arguably stronger than it has ever been, but it’s mostly priced in. The bear case is real but requires specific catalysts to manifest. The base case that Rocket Lab is a strong company executing well and a stretched valuation supports the current price. It does not necessarily support significant further multiple expansion from here.

This is the kind of company where the next 12 months matter much more than the previous 12. Neutron’s first flight, the Q2 and Q3 earnings prints, and the Golden Dome program flow will tell us whether the $120+ per share is a floor or a ceiling. Until then, every Rocket Lab holder is being asked the same question: Do you believe the execution risk is worth the price you are paying for the optionality?